Contributed by: Geetanjli Aggarwal

Email ID : geetanjali@simplybiz.in

Legal Requirements, Practical Insights & ADT-1 Filing Challenges

Overview

Once a company gets incorporated, the post-incorporation compliances form the foundation of a company’s legal and financial governance framework. One of the earliest and most critical compliances is the appointment of the First Auditor.

The appointment of the first auditor ensures:

- Financial transparency from inception by proper audit and verification of financial records

- Compliance with statutory accounting requirements

- Credibility with stakeholders and investors

Without a duly appointed auditor, a Company cannot legally finalize and audit its financial statements.

This article provides a comprehensive overview of:

- Legal provisions governing first auditor appointment

- Applicable timelines

- Requirement of filing Form ADT-1

- Practical issues currently being faced on the MCA portal

- MCA system limitations resulting in additional filing fees

Legal Framework

Applicable Provision

The appointment of the first auditor is governed by Section 139(6) of the Companies Act, 2013.

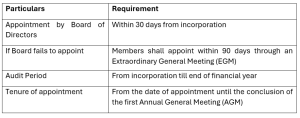

Timeline for Appointment

Is Appointment of First Auditor Mandatory?

Yes. Appointment of the first auditor within the prescribed timeline is mandatory under Section 139(6) of the Companies Act, 2013.

Failure to comply may attract penal provisions under Section 147 of the Companies Act, 2013.

Penalty Provision – Section 147(1)

If a company contravenes the provisions of Sections 139 to 146:

- The company may be liable to a fine ranging from ₹25,000 to ₹5,00,000

- Every officer in default may be liable to a fine ranging from ₹10,000 to ₹1,00,000

Accordingly, Companies should ensure timely appointment of the first auditor immediately after incorporation.

Requirement to File Form ADT-1

Form ADT-1 is filed with the Registrar of Companies (ROC) for intimating the appointment of an auditor.

The form is generally filed:

- Pursuant to appointment under Section 139(1)

- Upon re-appointment of auditor

- In case of change in auditor due to resignation or completion of tenure

The form is required to be filed within 15 days from the date of appointment.

Is ADT-1 Mandatory for First Auditor Appointment?

There has been a long-standing interpretational position that filing Form ADT-1 is not mandatory for appointment of the first auditor under Section 139(6).

This view is primarily based on:

- Rule 4(2) of the Companies (Audit and Auditors) Rules, 2014

- Which specifically refers to auditor appointments under Section 139(1)

- And does not expressly cover appointments under Section 139(6)

Therefore, legally:

- Filing ADT-1 for first auditor appointment is not mandatory

- However, many professionals still recommend filing it as a matter of good governance and record maintenance

Is Appointment of First Auditor Mandatory?

Yes. Appointment of the first auditor within the prescribed timeline is mandatory under Section 139(6) of the Companies Act, 2013.

Failure to comply may attract penal provisions under Section 147 of the Companies Act, 2013.

Penalty Provision – Section 147(1)

If a company contravenes the provisions of Sections 139 to 146:

- The company may be liable to a fine ranging from ₹25,000 to ₹5,00,000

- Every officer in default may be liable to a fine ranging from ₹10,000 to ₹1,00,000

Accordingly, Companies should ensure timely appointment of the first auditor immediately after incorporation.

Requirement to File Form ADT-1

Form ADT-1 is filed with the Registrar of Companies (ROC) for intimating the appointment of an auditor.

The form is generally filed:

- Pursuant to appointment under Section 139(1)

- Upon re-appointment of auditor

- In case of change in auditor due to resignation or completion of tenure

The form is required to be filed within 15 days from the date of appointment.

Is ADT-1 Mandatory for First Auditor Appointment?

There has been a long-standing interpretational position that filing Form ADT-1 is not mandatory for appointment of the first auditor under Section 139(6).

This view is primarily based on:

- Rule 4(2) of the Companies (Audit and Auditors) Rules, 2014

- Which specifically refers to auditor appointments under Section 139(1)

- And does not expressly cover appointments under Section 139(6)

Therefore, legally:

- Filing ADT-1 for first auditor appointment is not mandatory

- However, many professionals still recommend filing it as a matter of good governance and record maintenance

Practical Challenge: Additional Fees in ADT-1 Filing

Recently, companies have been facing a significant practical issue while filing Form ADT-1 for first auditor appointments made through an EGM.

Issue Observed

Where:

- the Board does not appoint the first auditor within 30 days, and

- the auditor is subsequently appointed by members within the valid 90-day period through an EGM, the MCA system is still levying additional filing fees while filing ADT-1.

Reason Behind the Issue

Based on discussions with the MCA Helpdesk, the issue arises due to system-level limitations in the ADT-1 form functionality.

Current System Logic

The ADT-1 form presently categorizes the purpose as:

“First Auditor by Board of Directors / Members / C&AG”

However:

- The system automatically calculates the due date as 30 days from incorporation

- The form does not contain any field to capture the date of the EGM

- Consequently, the system fails to recognize valid appointments made by members within the permitted 90-day period

As a result, additional fees are being auto calculated despite the appointment being legally valid.

Practical Illustration

Case Study

A private limited company was incorporated on 14 January 2026.

- The Board could not appoint the first auditor within 30 days i.e.by 13th February 2026

- Accordingly, the company appointed the first auditor through an EGM held on 31st March 2026

- The appointment was well within the permissible 90-day timeline under Section 139(6)

Thereafter:

- Form ADT-1 was attempted to be filed within 15 days from the EGM i.e. 14th April,April 2026

- However, the MCA portal reflected additional filing fees due to the system driven logic mentioned above

Professional Interpretation

The matter was also discussed with the Chartered Accountant proposed to be appointed as the first auditor.

It was confirmed that:

- The appointment had been validly made within the timelines prescribed under Section 139(6)

- Filing of ADT-1 is not mandatory for first auditor appointment under the Act

- The additional fees reflected on the MCA portal are purely system-generated and do not override the legal position

Accordingly, where the appointment itself is legally compliant, non-filing of ADT-1 should not be construed as non-compliance under the Companies Act, 2013.

Conclusion

Situations where the first auditor is validly appointed through an Extraordinary General Meeting within the statutory 90-day timeline prescribed under Section 139(6) of the Companies Act, 2013, the levy of additional fees on Form ADT-1 due to MCA portal limitations should be viewed as a technical and procedural issue rather than a legal non-compliance.

Since the Companies Act, 2013 and the applicable rules do not expressly mandate filing of Form ADT-1 for appointment of the first auditor, companies may take a practical and informed decision on whether to proceed with such filing, especially where additional fees are system-generated despite timely compliance with the law.

Leave A Comment